Blockchain: a Beginner’s Guide to Understanding This Revolutionary Technology

Welcome to the exciting world of blockchain! If you’ve ever wondered what this revolutionary technology…

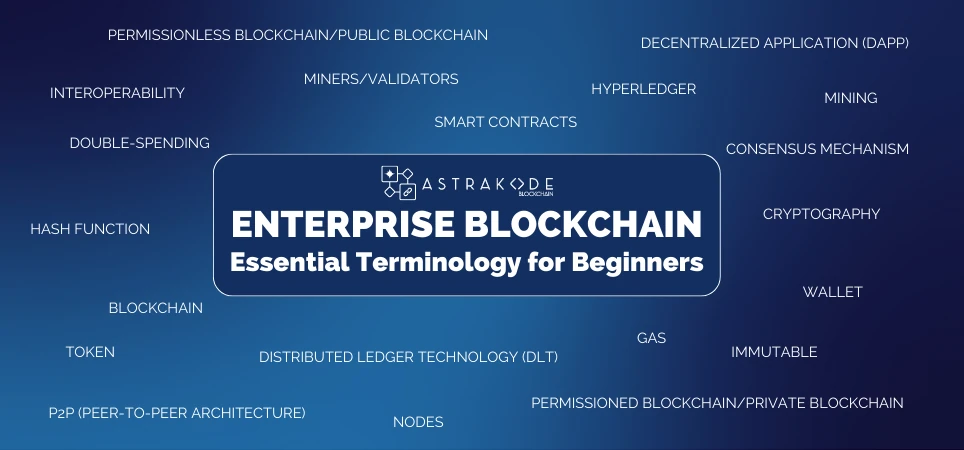

Are you a small business owner who is wondering whether to adopt blockchain technology? Or, maybe you’re a developer struggling to keep up with blockchain terminology. If so, you’re in the right place! This article will introduce you to 20 crucial terms related to enterprise blockchain and explain its significance for businesses.

The blockchain is a revolutionary technology that operates as a decentralized and distributed ledger, enabling secure and efficient recording and tracking of transactions and data across a network of computers. Its records are securely linked together through advanced cryptographic algorithms, ensuring the integrity and immutability of the information stored on the blockchain.

Distributed Ledger Technology (DLT) is a broad term used to describe a type of database that is decentralized and records information across a network of computers. DLT is different from traditional databases in that it does not have a central authority that controls the database. Instead, it is operated by a network of nodes that work together to validate and record transactions. This means that the database is more resilient to attacks or failures, as there is no single point of failure. Moreover, DLT finds application in diverse areas like supply chain management, financial services, and healthcare. With its capacity to enhance security, transparency, and efficiency, DLT is positioned to transform information storage and sharing in the future.

Smart Contracts are a type of digital contract that run on blockchain technology. They are self-executing contracts where the terms of the agreement between the buyer and seller are directly written into lines of code. A smart contract is a software program that, when triggered, automatically executes instructions to transfer tokens. These contracts are tamper-proof, secure, and enforceable. They have the potential to revolutionize the way we conduct business by reducing the need for intermediaries, increasing efficiency, and improving transparency. Smart contracts enable parties to automate complex processes and transactions, reducing the possibility of human error and fraud. They are already finding applications in diverse industries such as finance, real estate, and healthcare, holding the potential to revolutionize future business practices.

Hyperledger is an open-source project that aims to create enterprise-grade, distributed ledger frameworks and code bases. The project is focused on developing blockchain technology solutions that can be used in various industries such as finance, healthcare, and supply chain management. One of the key objectives of Hyperledger is to make it easier for businesses to adopt blockchain technology by providing a set of common tools, standards, and libraries that can be used to build blockchain-based solutions.

The consensus mechanism is a vital component of blockchain networks, as it guarantees that all nodes reach a mutually agreed-upon state of the blockchain. This process eliminates the need for a central authority and ensures that transactions are valid while preventing double-spending.

Double-spending is a dangerous phenomenon where a person can replicate and reuse electronic transactions such as payments. Cryptocurrencies are especially at risk of double-spending because a modification of transaction information within a blockchain can enable the use of the same coin multiple times. This vulnerability can allow the initiator of the alteration to reclaim spent coins if certain conditions are met. In other words, if modified blocks enter the blockchain, the person who made the alteration can exploit the system.

Network participants known as miners or validators play a crucial role in validating transactions on the blockchain and preventing double-spending. Miners operate cryptocurrency mining equipment to solve intricate cryptographic problems and add the next block to a blockchain. This effort earns them block rewards and transaction fees through the consensus process called proof of work (PoW), recognized for its stability and effectiveness despite its energy intensity. In contrast, validators in proof of stake (PoS) networks stake a specific amount of digital tokens to partake in validation, bypassing the need for mining equipment. This approach curtails costs and risks related to mining, making it more accessible to anyone meeting minimum token requirements. Both miners and validators are crucial for maintaining the integrity and security of blockchain networks.

Mining is a crucial process in the blockchain network, as it enables the creation of new blocks and the verification of transactions within the blockchain. Powerful computers are employed by miners to solve intricate mathematical algorithms, and after verifying a block, it’s incorporated into the blockchain. This process guarantees the security and immutability of the blockchain network, as each added block becomes permanent and remains unalterable or deletable. This is a key feature of blockchain technology, as it provides a decentralized and transparent system for recording and tracking transactions.

Nodes are computers connected to a blockchain network that validate and verify transactions. They are responsible for validating and verifying transactions on the network, ensuring the integrity and security of the blockchain. In basic language, a node is a computer connected to a blockchain network, responsible for tasks like transaction verification, data storage, and network security maintenance.

A hash function is a mathematical function that converts an input into a fixed-size output. It converts data of any size into a fixed-size output, known as a hash value or digest. This hash value is unique to the input data and is used to verify the integrity and authenticity of the data on the blockchain. Hash functions are one-way functions, meaning that once the data is hashed, it cannot be reversed back to its original form. This makes it impossible for anyone to tamper with the data on the blockchain without being detected.

Immutable data refers to information stored on a blockchain that cannot be altered or deleted. This embodies a core trait of blockchain technology, guaranteeing that once information is recorded on the blockchain, it remains unalterable and immune to deletion by any entity. This feature makes blockchain an ideal solution for industries that require secure and tamper-proof data storage, such as healthcare and pharmaceuticals

Cryptography is the science of encrypting and decrypting information to secure it from unauthorized access. In blockchain, it protects transactions between two nodes in the network. Two main concepts in blockchain cryptography are cryptography and hashing. Cryptography encrypts messages in the P2P network, while hashing secures block information and links blocks in the blockchain.Cryptography is crucial in maintaining the security of the public network, making it suitable for maintaining the integrity and security of the blockchain.

A token is an embodiment of ownership for a digital or physical asset that is tradable. The token functions as a cryptographic representation of digital possession and securely stores on the blockchain. This is achieved by encoding explicit rules into the corresponding smart contract linked with the token. The blockchain address links to each token, ensuring legitimate ownership and distribution. Though often linked with cryptocurrencies like Bitcoin and Ethereum, tokens possess diverse roles. They can signify voting rights, software licenses, or ownership of creative works. Their function is to authorize permission and/or ownership for users, playing a crucial role in enabling blockchain technology’s functionality.

Peer-to-peer architecture is a highly efficient and innovative technology that operates on the principle of decentralization. By eliminating the need for a centralized authority, P2P enables nodes to directly share and access resources with each other, resulting in increased speed and ease of access.

A digital wallet stores your private keys and enables you to interact with a blockchain network. It is essential for cryptocurrency transactions, balance viewing, and blockchain participation. Beyond cryptocurrency, it can manage non-fungible tokens (NFTs) and digital assets. These wallets ensure secure storage, easy management, and access to the blockchain network.

Gas represents the cryptocurrency fee for executing a transaction on the blockchain. On the Ethereum platform, gas is essential for successful transaction or contract execution. The fees are denoted in minute fractions of ether (ETH), known as gwei (10^-9 ETH). Validators receive gas as payment for the resources involved in transaction processing.

A decentralized application, or DApp, is a unique type of application that runs on a blockchain network and utilizes smart contracts. Unlike traditional applications, DApps are built on a decentralized architecture that allows them to operate without a central authority or intermediary. DApps have been utilized in decentralized finance (DeFi), where they perform financial functions on blockchains. Decentralized finance validates peer-to-peer transactions to disrupt centralized finance and reduce costs. Each DApp has an identifying code that may only work on a specific platform.

In the context of blockchain, interoperability specifically refers to the ability of blockchains to communicate with each other. This is achieved through cross-chain messaging protocols, which allow blockchains to read and/or write data to other blockchains.Cross-chain messaging protocols support the creation of cross-chain decentralized applications (dApps). These dApps function across multiple smart contracts that are deployed on different blockchains. In contrast, multi-chain dApps deploy on multiple blockchains, but each instance constitutes an isolated set of smart contracts with no connection to other blockchains.

A permissioned blockchain mandates explicit participant permission for network access and engagement, unlike public blockchain networks that welcome all participants unrestrictedly. Industries needing controlled and restricted data access often utilize permissioned blockchains. For instance, in healthcare, they secure sensitive medical records access solely for authorized personnel. Similarly, finance leverages permissioned blockchains to restrict fund access and transfer to authorized parties. A paramount benefit of permissioned blockchains is their elevated security and privacy compared to public counterparts. Since the network is only accessible to authorized parties, there is less risk of unauthorized access or a malicious attack. This makes permissioned blockchain networks ideal for industries that require a high level of security and privacy.

A permissionless blockchain operates on a decentralized network, welcoming anyone to join, participate, and contribute without seeking permission from a central authority. This openness fosters heightened security, transparency, and immutability as a multitude of nodes uphold the network, deterring tampering. This decentralized setup fosters innovation and creativity, enabling the development of applications, smart contracts, and decentralized organizations without constraints. In essence, permissionless blockchains hold the potential to revolutionize industries by enabling decentralized applications and services.

Enterprise blockchain technology has the potential to fundamentally transform the way businesses operate, offering a wide range of benefits that include cost reduction, increased efficiency and security, and enhanced transparency. By embracing blockchain solutions, companies can optimize their processes, streamline transactions, and eliminate intermediaries, leading to quicker and more cost-effective outcomes.

However, the implementation of blockchain solutions can be a complex and time-consuming process, particularly for smaller organizations. That’s why low-code solutions like AstraKode Blockchain offer an ideal solution. AstraKode Blockchain empowers businesses to effortlessly construct secure and efficient blockchain networks, utilizing Hyperledger and Smart Contracts in Solidity, all without the need for coding expertise. This enables businesses to focus on their core operations while still being able to leverage the benefits of blockchain technology. By providing a simple and effective solution for blockchain implementation, AstraKode Blockchain allows you to simultaneously save time, effort, and money. Sign up now and start your journey!

To conclude, enterprise blockchain technology undeniably represents the business future, delivering cost-saving advantages, heightened efficiency and security, and increased transparency. Nevertheless, embracing blockchain solutions, particularly for small businesses, can be daunting. Yet, low-code solutions like AstraKode Blockchain offer an efficient pathway for businesses to tap into blockchain’s benefits without substantial development investment. We believe this article has enhanced your comprehension of key terms in enterprise blockchain and its potential to empower your business.

Welcome to the exciting world of blockchain! If you’ve ever wondered what this revolutionary technology…

Blockchain technology has taken the world by storm and has become a vital tool in…

Sharing documents is a common practice in business, but the advent of blockchain technology has…